What Is Going On?

- silver and gold are having their worst week in 3 years

- the dollar is strong on the back of the unresolved EU banking crisis and Fed hike talks

- oil, and the nikkei are strong

Background

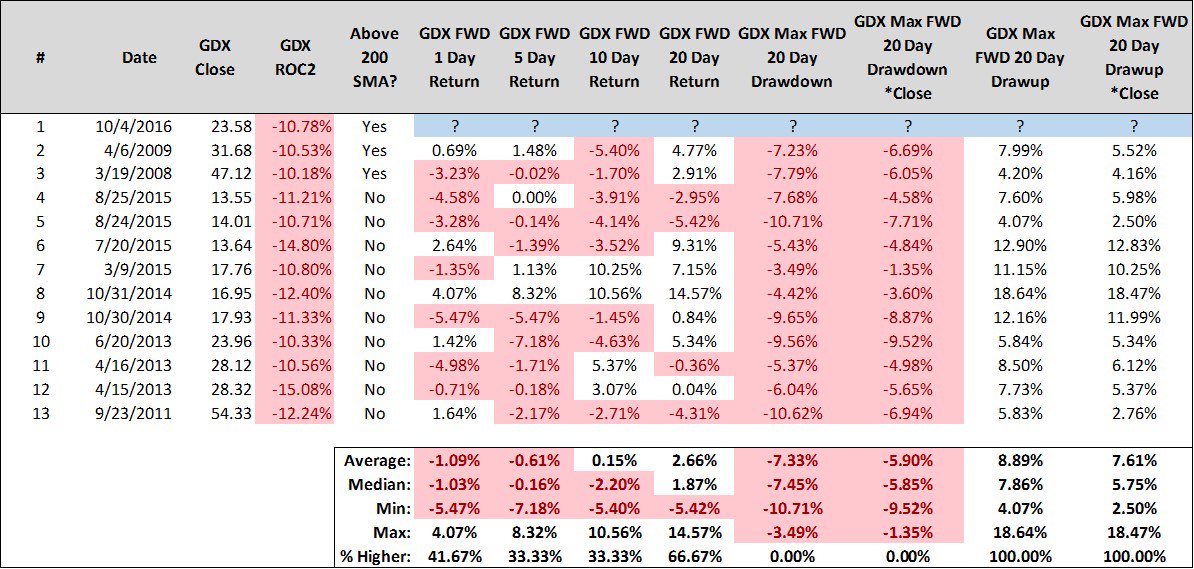

Since our last post, Gold is now below every technical level we have to still call this a bull market, including the 200 DMA. Only the $1155 level remains as the 67% retracement level from the beginning of this whole rally.

TUESDAY

Full Post HERE

The only indicator we had to not buy the dip turned out to be spot on. It was an analysis of ifthe GDX was a buy after its 9.8% drop on Tuesday

FTA - Buying GDX? Not So Fast

Overview

Precious Metals are getting decimated this week. We have not forgotten, nor are we burying our heads in the sand tempting as that may be. Right now people feel like mushrooms: Kept in the dark and fed a load of crap. We have no desire to fill space with empty rhetoric that does nothing to help an investor get a handle on what is truly going on. And have waited until something that made sense drew our attention.

Someone Is Being Forced to Liquidate

Absent information and any reliable correlations in the marketplace we have only one conclusion: Forced Liquidation. It may be a function of performance, scandal, or government involvement. We do not know. But someone is being liquidated. If a scandal does not rear its head in the next few days, we are placing our bets on over-leverage as the reason for the liquidation. Using the assumption that the market moves are not fundamentally driven or a product of CB policies ( directly), the moves are for a non-macro reason. What else has moved?

What Else is Moving

- There is massive FX volatility as money piles into the USD

- Oil is rallying relentlessly

- Gold is down against every major currency this week

- There is no observable news to justify moves of this magnitude

- Precious Metals are having the largest drawdowns of any other market

- JGBs after getting hammered post the BOJ August policy change have recouped 1/2 of their losses

Right now we are trying to get a bearing on the possible causes seen and unseen on the deluge of selling.

In times like this, we are long on observable facts, and short on opinions until a thesis that ties things together materializes. And when one does not, we just look at what is moving the most and try to reverse engineer the behavior.

Biggest Movers This Week

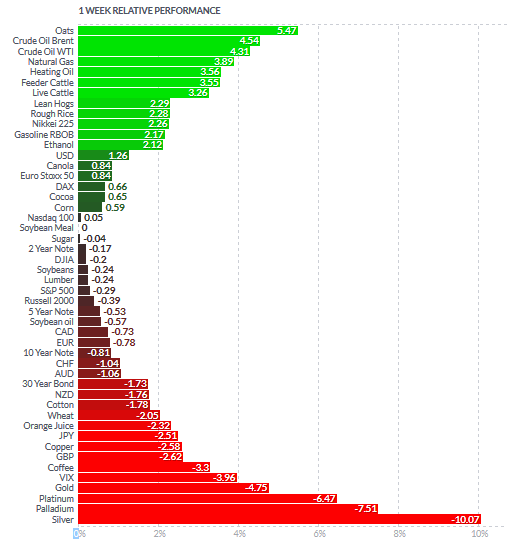

Using the chart below we can easily spot what the biggest movers in widely held commodities and the FX markets were this week.

Weekly Futures Performance

Biggest Movers By Category

- Precious Metals: Silver, PGMs, and Gold down the most in that order

- Currencies: GBP, JPY, down the most; USD up the most

- Energy: Oil, Nat Gas, up the most

- Equities: Nikkei up the most

- Gov't Bonds: JGB's very volatile (down in august) back up in September at end of 3rd quarter

Hypothesis: Forced Total Liquidation of an Entity

- the moves in all the markets described above are possibly due to an exogenous factor rather than the merits of the investments themselves.

- In the past, when the dust settled, the cause was either

- a scandal like the BCCI Silver or Sumitomo Copper scandals

- a large end of quarter redemption forcing a Hedge Fund to liquidate- Leverage (LTCM), Investigation (PPVA) or underperformance as instigators

Regardless of the reason behind the markets' behaviors, Forced Total Liquidation means a portfolio's winners are closed in conjunction with its losers. Additionally, all it takes is one fund that is long Gold and short JGBs to start the ball rolling because of a forced liquidation. The next fund to puke can be long gold and short oil.

In fact, if once were to view the levered Hedge Fund industry as one large fund, and knew which asset all had in common in their portfolios, it could only take a push on that one asset to take down a whole financial segment. it would seem the positions most widely held by leveraged funds are short dollars, and short JGBs. The asset that theoretically and quite practically suffers the most from a rush to the exits is Gold, the smallest, yet most widely held in the levered fund industry.

Who?

We don't know. But the FT's Miles Johnson recently wrote about the Odey Fund:

"many financial commentators have warned that current monetary policy has inflated a bubble that will one day violently pop. Few of them have risked money betting on the precise manner in which a chaotic unwinding of quantitative easing will play out through financial markets. This makes the portfolio of Crispin Odey, a London-based hedge fund manager, an interesting outlier. Mr. Odey is one of only a handful of investors who has backed up his dire prognosis for the global economy with a series of large, leveraged trades designed to pay off in the event of a crash."

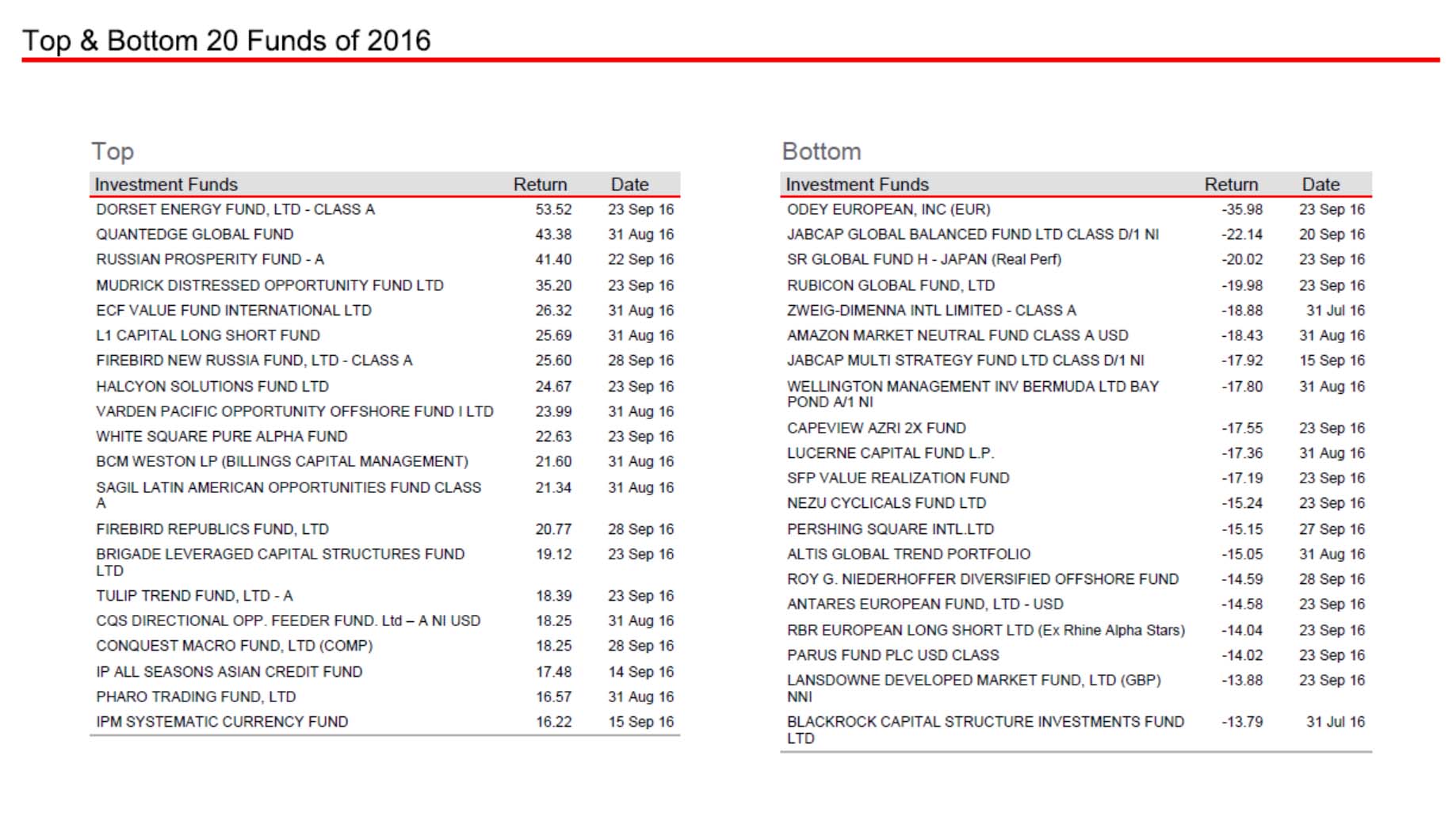

Crispin Odey's Fund performance YTD as Q3 Came to an End

Why?

Sticking with the Odey fund. Crispin Odey has bet that Bonds will drop, and that global currencies will devalue. His Bonds of choice are JGBs (and Gilts) of which he is short. His choice instrument in expressing his Fiat currency bearishness is in Gold, which he is long. His bearish plays on equities are smaller. Not being long is enough these days we guess!

But it is not the opinion or even the postions that Odey has, it is the leverage that is the risk.

ODEY's Levered Gold Bet

Odey’s biggest bet is in Gold. Gold represents 100 per cent of his fund’s unleveraged value, meaning a large rally or fall in its value may dictate the fate of his entire portfolio. His reasons are well known, and may be why he has become a target if it is Odey being liquidated. Mr. Odey: “central banks have printed $80tn of money, backed by only $1.27tn of gold”. Which we agree is going to be the death of all paper money. But to be leveraged to the extent that Odey is may be irresponsible.

As the FT states: "Odey’s long gold position interacts with his overarching premise — that a crisis starting in China explodes through global markets. Large amounts of global gold demand come from Asia."

And there is the problem. The crisis has to be inflationary, not deflationary. And Central Bankers are in charge of a market that will take out leveraged portfolios despite easy money.

ODEY's Levered JGB Bet

Mr Odey’s second big trade is that Japanese government bond yields will explode higher as financial markets realize that the “all in” Bank of Japan has run out of ammunition. Some macro hedge funds have over the years attempted to short JGBs based on the idea that the country’s indebtedness and poor growth was incompatible with its low yields. JGB yields have continued to drop, leading to the trade being nicknamed the “widow maker”

Again from the FT:

"the premise that JGB yields will rise during market turmoil is no certainty. The Japanese are the world’s largest single owners of financial assets, which in the event of a crash would presumably be sold and funds repatriated into yen. Over the last two decades a strong yen has tended to coincide with a fall in Japanese government bond yields. Betting against JGBs in anticipation of a crisis may have painfully opposite consequences when a crisis arrives."

When does it end? - The trigger event may be over already. We may now be seeing secondary liquidations of smaller, less deep funds that have similar positions.

Implications?- If this is indeed a Forced Liquidation Event, it will damage the Metals market psychology for some time. Not only will "hot" money stay away from the long side, but deep pocketed investors will as well, noting the lack of exit liquidity available in times of duress.

Where is the Good News?- unless Central Banks step in and start competing against each other to buy aggressively, there is none for now. It would be good news if a Fund that got overextended in its positions was the reason that the market sold off. That would be an irrational sale and not invalidate Gold as an investment and monetary alternative. But it would scare away otherwise rational people as well who do not play the leverage game.

Dennis Gartman Weighs In

Mr. Gartman receives much criticism for his market calls, especially in oil. But that said, we have seen him make some very good calls over the last 20 years. And almost exclusively, when he is right on Metals, his sources and information are out of the London markets. So when he opines and makes it clear that he is channeling something someone in London confided in him, we listen.

"As for gold and the other precious metals they remain rather obviously weak and as we move away from Tuesday’s collapse it appears more and more that this was a forced liquidation on the part of a large… actually a massive… hedge fund out of London. The sheer panic that swept through the gold market then really hadn’t the look of a sell off predicated upon a rumoured push by the ECB to curtail its purchases of sovereign debt securities, nor had it the look of a rush on the part of hedgers in the gold mining industry to hedge forward production. Rather it had the look of forced margin-clerk liquidation. It looked like panic on the part of someone, somewhere who had lost control of the situation."

We have seen lucid, well thought out comments from Mr. Gartman before, like when the Silver spreads went into backwardation in 2011 during London hours. These type of statements we do not fade or discount as being contrarian indicators. Especially when he is not giving a directional opinion. But was looking for color on why Gold (a position he held) sold off.

The Lesson for Us, and maybe for ODEY

The "tell" which should have been obvious was the way markets reacted when the Deutsche Bank crisis escalated.

- Gold should have screamed higher- it did not

- the whole of the EU equity markets should have washed out- it did not, just the banking sector

- The US Fed did not back off its "rate hike" chatter despite the DB crisis and the stronger USD

- The BOJ policy change to taper their buying of bonds should have been more damaging to JGBs- they were not

The axiom "If your position does not perform well on bullish news, you should expect to perform horribly on bearish news" would seem to apply here.

Good Luck

Read more by Soren K.Group