Why Gold Bulls Should Want a Rate Hike- Analysis

UPDATE: 10/04/16

-Soren K

This article, written by our friend Vince Lanci is still applicable, and almost prescient in its expectations. We thought it appropriate to feature again. In it he lays out a potential play by play for the next crisis' creation and solution. Included is Deutsche Bank's own feel for the next round of QE. Note how DB called (begged?)for it well in advance of their own crisis. We imagine they will be the first in line if the ECB bails out the Banks again. Here's to hoping!

This last week's drubbing in precious metals has left many scratching their heads, and we are no exception. A reality check is in order before we hold hands and tell each other everything is all right

- This Precious Metals bull market is in serious danger of being dead

- Below $1290 is definite hospitalization

- Under $1270 on a weekly basis is good for critical condition

- Below $1155 and there is nothing left to even rationalize.

Fund Traders Weep while Central Bankers Sleep.

"Bull market" is a term for traders. The investors, namely central banks, will be stepping in with both hands buying physical now. We see physical demand in both metals already coming in on the buy-side today. Does that mean we are going up? NO. It means that deep pockets, who are a lot more patient than they used to be are starting to pick their levels.

They will let the market come to them as long funds and banks puke. Then they will let it go lower as momentum funds start so sell it in the hole. Then when the OI is solidly short on the fund side, they will keep buying. And when the natural sellers and spec sellers are done, the physical guys will slowly start to raise their bids.

And THEN you will see the rally as short funds start to cover.

Other than Central Banks you will see JPM in the Silver market. They are long a ton (or so) of physical silver. And when they see the flow turning bearish, they hedge it by selling futures. And when that market gets oversold, JPM is the buyer of spot in London for a profit. That is how it happens, always. And when bullion banks see vulnerability in the Metals, they will get short on top of their paper flat position. Their core short trading position are put on from selling strength. They will sell weakness in a thin market. Sometimes to trigger stops for a washout. Sometimes to cover their own shorts as they see the tide beginning to turn bullish again. Spoofed markets lower are somethimes to trigger cascading selloffs, and sometimes to create an exit for a player to cover shorts.

The Point is: Deep pockets buy low and high. Shallow pockets use leverage and buy high and hope to sell higher.

FWIW

We are bidding on Silver in small amounts for personal use 5-10 years form now. We are using its crazy volatility to buy extremes. We are NOT selling it. We are giving it to our children when they hit college.We aer not deep pockets by any means. But we are aware of what we need to live on financially, and what we can buy and hold for 5 years for our children to use.

Vince's Play by Play, with caveats starts in "Global Helicopter Squadrons and Currency Drainage" subsection below.

Related Today:

- Technicals: $1290 is a Line in the Sand, Here's THE Line

- Top Day: USD, Gold Eye Fed, Deficit Climbs $1.4 Trillion in 2016

The Fed is Out of Ammo

While the markets gyrate against a backdrop of the Fed symposium Jackson Hole jawboning it might be prudent to put ourselves in the Fed's shoes for a moment.We do think the Fed is constrained from doing the right thing even when it wants to by political pressures. An outgoing Democrat POTUS and the current front runner, Hillary Clinton have major stakes in the stock market price as a "legitimate" barometer of the economy. It would be far tougher for Mrs. Clinton to win if the S&P were 500 lower. There would be nothing to hide behind when the populist revolt swelled and attacked their policies head on. Trump could win. Add to that the reality that the economy has not recovered, the newly employed are waiters and bartenders (who are now getting laid off) and it seems ludicrous to raise rates.

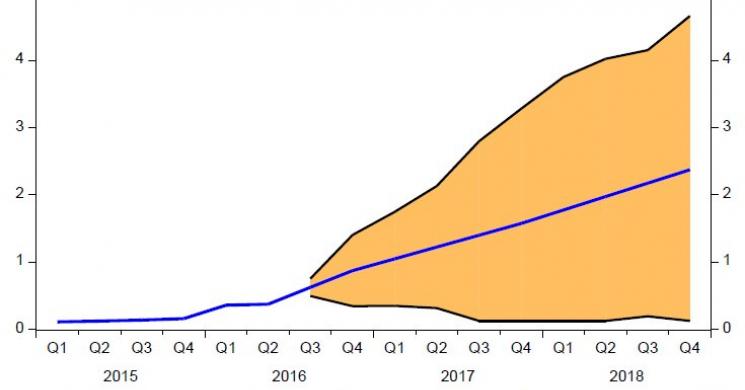

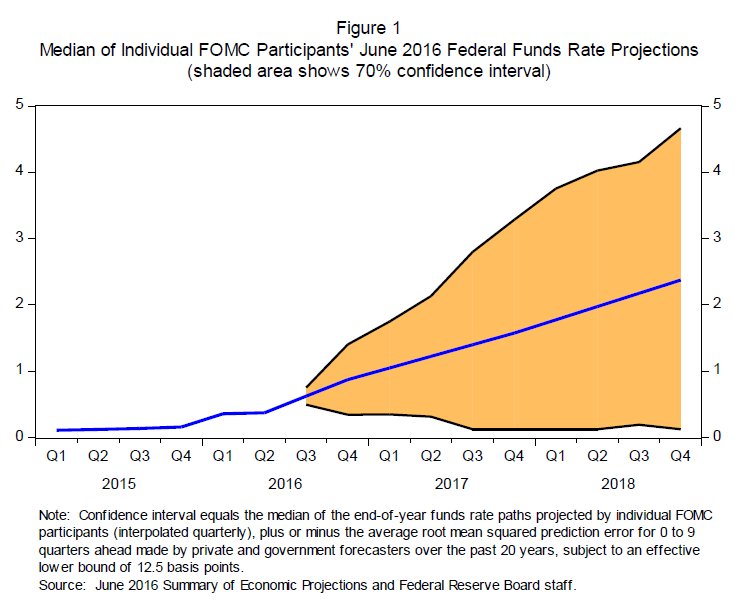

On the flip side, what can the Fed materially do if there is another crisis? Pretty much nothing. They have no ammo. This is reflected somewhat in Janet Yellen's speech which gives a rather wide berth for rates in 2018.

"The shaded region, which is based on the historical accuracy of private and government forecasters, shows a 70 percent probability that the federal funds rate will be between 0 and 3-1/4 percent at the end of next year and between 0 and 4-1/2 percent at the end of 2018.2 The reason for the wide range is that the economy is frequently buffeted by shocks and thus rarely evolves as predicted. When shocks occur and the economic outlook changes, monetary policy needs to adjust. What we do know, however, is that we want a policy toolkit that will allow us to respond to a wide range of possible conditions."

Note the last sentence. That is basically an admission that they have no bullets to use if there were another crisis. The only way to have anything in reserve for a crisis event is to reload the gun by raising rates. And by the way, a 70% probability is not very good. That is 1 standard deviation from where we stand in a world where 3 STD moves are becoming not the norm, but the reaction to almost any exogenous shock in other markets.

- Norway's Bank Brings Home Gold- but that's not our business

- Kuroda at Jackson Hole Saturday: “Zero lower bound is no longer insurmountable in practice"

- CHARTS: on QE, Barney Frank's plea, RIP German austerity, ECB's spending spree

- THE CASE FOR UNENCUMBERING INTEREST RATE POLICY AT THE ZERO BOUND- paper

How to Reload?

So how can one reconcile the potential disastrous effects of a rate hike on: the election, the stock market, and the actual economy with the need to be ready for a crisis? The answer for us is simple but not easily done. Create the crisis by raising rates. This may sound conspiratorial, but we are not saying that the Fed wants to create a crisis. We are saying that the Fed wants to fix the economy. And though one may think its efforts may be compromised and wrong, those in the FOMC believe their own intentions. And to that we say, they have to raise rates at some point soon. And when they do, it will create the crisis they need to convince the world that QE and more is the only answer.

You Gotta Bid to Sell

The title of this section is an old quote from traders who used to say, " If you want someone to buy from you, you have to bid first to get them to join you. Then you smack their bids. Otherwise how will you get exit liquidity? " Essentially the mechanics of spoofing, if you will. Raising rates might create the situation that is needed for another round of Quantitative Easing and likely some form of permanent debt monetization like "helicopter money". In our global scenario we have been seeing tells that QE and more is coming on a globally coordinated basis. We think ground zero for the implementation of Helicopter money being officially used will be in Japan. Remember when Bernanke made his trip to speak with Kuroda about a month or so ago? That was to get people on the same page while keeping the Fed at a perceived arm's length away.

So while we remain flexible on the tactics potentially employed, the strategy remains the same.

- The Fed needs monetary bullets in case of a crisis

- The USA will be the last to stop exporting its deflation and therefore the last to truly debase its currency via helicopter money.

Global Helicopter Squadrons and Currency Drainage

So how does it happen? We are not sure and are never married to the order of events. Being able to create tangents within a framework of concepts is easiest and keeps our thought process least biased. But right now it could go like this:

- Japan will start the ball rolling. Stocks and Gold will rally there in yen terms. Japan started this global deflationary cycle. They should be the first out of it.

- China will have to further accelerate its Yuan depreciation against the USD. Remember their reaction to the Brexit vote? China potentially lost a favorable link to the EU via its relationship with the UK

- The UK and EU will also then consider more QE and helicopter money. Their reasons will be different, but their actions will be the same. For the EU it will be to rescue Italian banks. For the UK, it will be to help their exporting commerce.

- There will be a "whiff" of inflation but no-one will pay much attention

- The US will be forced to capitulate on its own Fiscal stimulus citing the damage done to our economy by a strong dollar etc.

- Stocks, bonds and Gold will rally with Stocks outperforming everything in what should be a massive blowoff top for them and Bonds

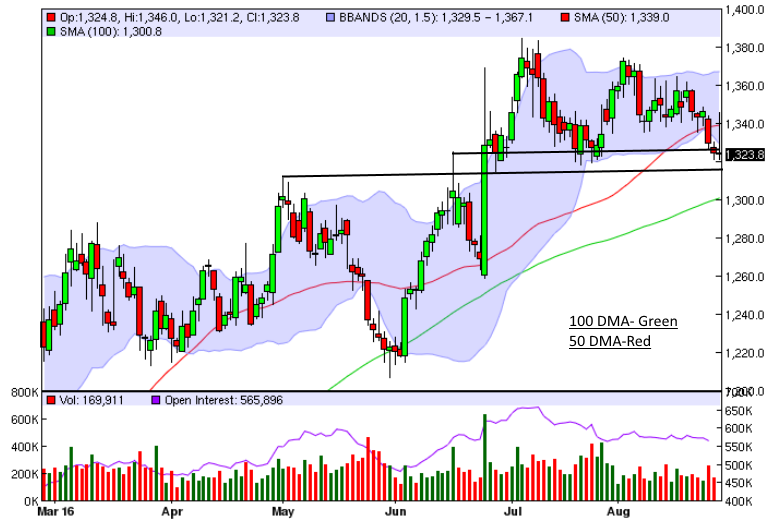

Gold Daily Chart

Interactive chart HERE

The Biggest Spoof Ever

Somewhere in that mix, the Fed will have to raise rates first. They will have to raise 25 basis points to lower 50 effectively and launch QE4. That is a tactical decision and we are sure there is some trigger for it. Perhaps it is the S&P above 2300. Perhaps it is a truly good economic release. But whatever the reason/excuse, the rate hike will cause the stock market and Gold to selloff. And that selloff will be at or near all time highs for stocks. So the market will be able to take that hit for a while. Conversely, gold will not be at all time highs, meaning the Fed has done its job in their minds. And then you get QE4 and turbo money. You gotta bid to sell indeed.

Then we get inflation. The kind you cant cure just by raising rates. For a proxy on the Fed's future inflation-fighting prowess, just look at what lowering rates for 10 years has done for deflation. Why do they think they can stop it once it starts so quickly?

Here's Deutsche Bank's rationale for what we are attempting to describe. DB would be first inline as a bank in need of money, so their pitch isn't objective by any means. But who's is?

Originally posted in Zerohedge.

So, for those who care, here is Deutsche Bank's elevator pitch for why helicopter money should be next:

- We have evolved to the point where familiarity with QE breeds acceptance, while unfamiliar ‘helicopter money’ policy, unfairly breeds contempt.

- Compared with the scale of QE liquidity dropped into financial institutions, piling up in the form of excess reserves, the exante and expost calibration of Helicopter money can be considered almost surgical. Helicopter money legacy issues are miniscule compared with the QE overhang of liquidity in the system, and a costly and bloated Central bank balance sheet, which is so difficult to reverse.

- QE forces a substitution into riskier assets, which is another way of saying it inflates and distorts the price of risky and less risky assets, with implications for all balance sheets, and inter-temporal economic decisions. Helicopter money is less likely to distort every asset price in the economy, when compared with deliberate financial repressive policies like QE and negative rates.

- One of the big criticisms of helicopter money is that it is open to political abuse and that the coordination of fiscal and monetary policy, threatens Central Bank independence. This is less of a worry if there is a clear institutional framework whereby the Central Bank has the final say on whether to participate in any helicopter scheme or not, and they can ‘right size’ the stimulus.

- If one has to be cautious about Helicopter money it is less about whether it can be successful, and more about how in these times of excessive demand management, any effective tool is apt to be used to the point of abuse.

- Helicopter policy that successfully supports growth (with contemporaneous rightward shifts of the IS and LM curve) inclusive of favorable multiplier effects, will likely temporarily drive nominal interest rates higher, and the question for real interest rates (that with nominal rates is a key FX driver) is whether inflation expectations rise more rapidly than nominal rates.

- Carefully calibrated and contained Helicopter actions, by an independent and historically credible Central Bank (not an oxymoron), would likely have a contained impact on inflation expectations. This is especially true, if Helicopter money is pursued in emergency deflationary circumstances. As such, any initial kneejerk selling of a currency when a G10 country pursues a measured Helicopter solution that is befitting of its large disinflationary output gap, is likely to be a medium-term buy the currency dip opportunity.

- Because Helicopter money is less directed at using currency weakness as a core transmission mechanism than QE or particularly negative rates, Helicopter money should be more, rather than less acceptable to an international community worried about currency wars.

The Missing Piece

Our own thesis has been bearish stocks since last month. But this analysis has been haunting us in view of what was observed. Namely the global market reaction to Brexit, China accelerating its decoupling from the USD, Bernanke's Japan visit, Abe floating Helicopter money to the public, and the lack of need to do anything by the US Fed except keep dollar swaps liquid for EU countries.

What we couldn't figure out was how can the Fed do another QE with rates at zero? And the answer is, raise rates only after the Stock market is able to absorb a 200 point drop from all time highs. Cheat.

The Egress

Sadly, then you get constraints and higher taxes as the Government needs to feed itself while slowing the flight of capital into Gold. A VAT tax on Gold perhaps. Maybe a forced cash settlement on physical futures? A surtax on house sales like in Argentina? Certainly currency wars can then morph into global trade wars. And imagine if the China South Sea issue became a focal point during a stagflationary tradewar? on second thought, don't.

vbl

Good Luck

Read more by Soren K.Group