We realise that the ownership of gold is very emotional for many people and we want to assure all of our readers that our analysis is in no way meant to insult anyone. We are calculating probabilities NOT making prophecies. We can’t know the future, so we calculate according to what has happened in the past.

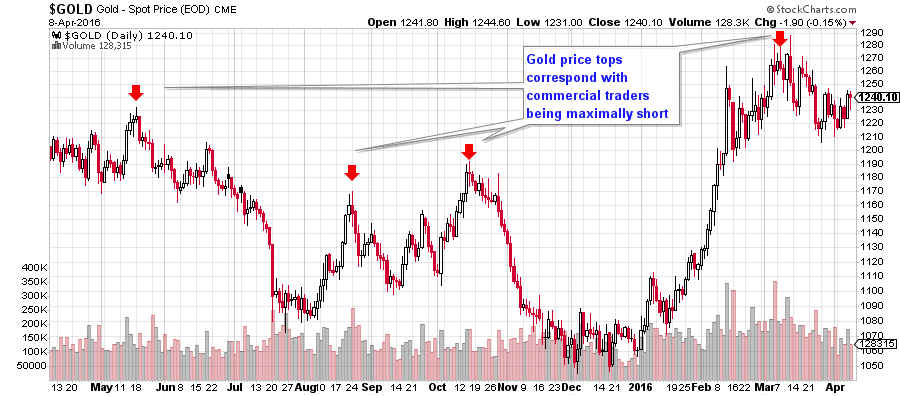

Gold has been range-bound between $1205 and $1250 for the last three weeks, but our probability calculation still weighs on the side of lower prices in the medium-time frame (three months).

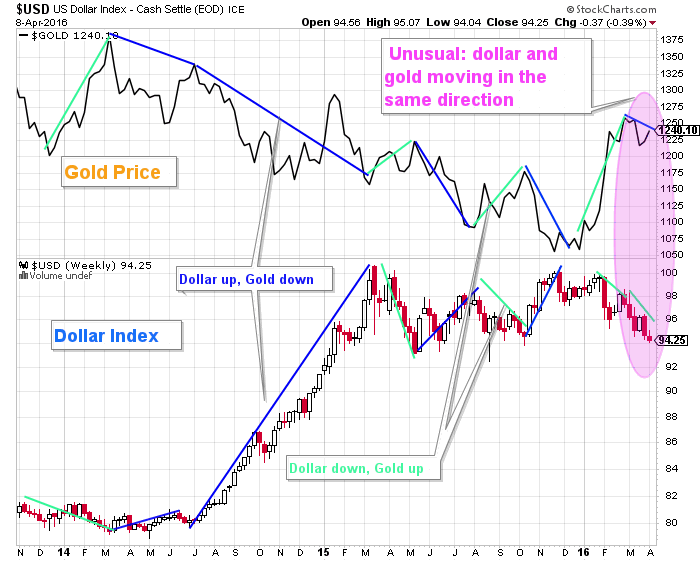

The chart below shows the relationship between the dollar index and the price of gold. The dollar index is influenced by the FED rate (as well as other factors, of course); as rates rise (or are anticipated to rise), the dollar tends to go up and, therefore, gold tends to go down (see chart).

Notice how frequently gold and the dollar move inversely to each other, and notice also that eight weeks ago, gold started to trade down, even as the dollar dropped. That demonstrates a lot of selling, and high-lights the weakness in gold—if it can’t sustain a rally while the dollar is slumping, then how is it going to fair against a strengthening dollar?

The dollar has been range-bound between 93 and 100 for the last twelve months, putting the odds on the side of another move back to the upper price-range. Once we get into May, the FED will have some interest in keeping June alive for a rate hike. The CME FED tool for the June 15th meeting shows a 21% probability of a 0.25-point rate hike, and this is likely to increase as the expectation becomes more wide spread. If the job numbers continue to show growth, and wages start to improve, then the FED would have enough cover to hike again. Even if they don’t hike in June, six weeks of expectation should be enough to get the dollar up.

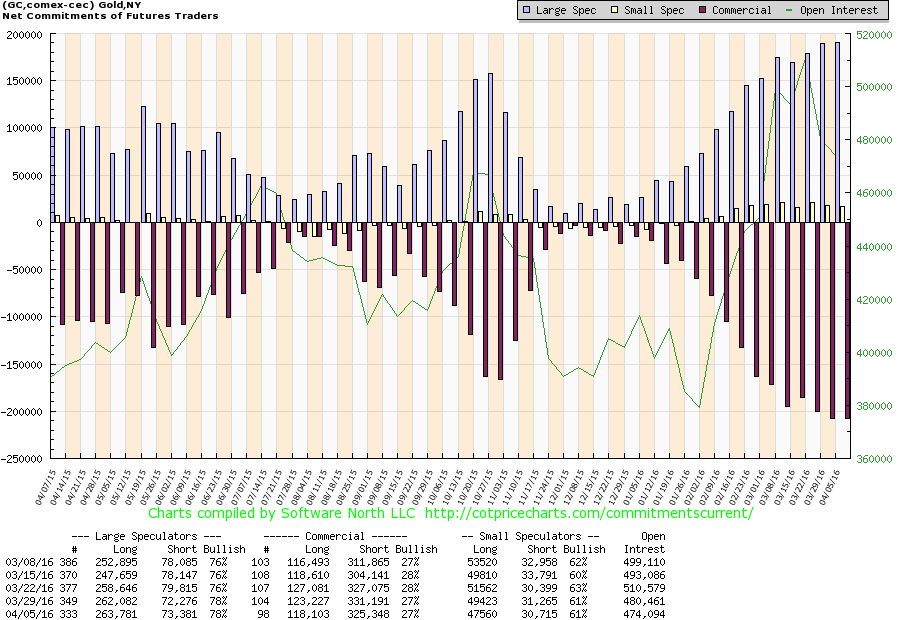

The commitment of gold futures traders (chart below) is still in an extremely bearish position; the large speculators increased their long positions again last week, and the commercials maintained the most extreme net short-position since 2011.

Could the commercials be wrong this time around? The answer, of course, is certainly they can. But the more appropriate question is, why would you want to bet against them now? What’s different this time?

{This section is for paid subscribers only}

ANG Traders

Join us at www.angtraders.com and replicate our traders and profits.

Read more by ANGTraders