One year ago, British voters cast their ballots in favor of leaving the 28-member European Union, defying multiple opinion polls leading up to the Brexit referendum that said the “remain” camp would notch a narrow victory.

In a pre-Brexit Frank Talk last year, I wrote that Brexit would be regarded as the most consequential political event of 2016. President Donald Trump’s surprise election notwithstanding, I stand by my earlier comment.

Brexit, in fact, laid the groundwork for Trump. Both movements, described by many observers as populist and nationalistic, exposed an impatience and frustration with rampant bureaucracy, strangulating regulations, lax border security, political correctness and a sense of a loss of autonomy. “Take our country back!” and “We want our country back!” were the battle cries of supporters of Trump and Nigel Farage, then-leader of the UK Independence Party (UKIP).

EU membership has been nothing if not costly. As I shared with you last year, the U.K. is the third-largest net contributor to the Brussels-based bloc after Germany and France, paying the equivalent of between $11 billion and $14 billion every year. On top of that, the 100 most expensive EU regulations, passed down by unelected officials, are estimated to cost somewhere in the vicinity of 33.3 billion pounds, or $49 billion.

Although the British economy is showing signs of slowing down, the country has not contracted or imploded as many Brexit opponents had predicted. In fact, certain British sectors such as exports and manufacturing continue to expand.

Further Reading on Brexit:

Where the Rubber Meets the Road

Now that the “leave” camp has its country back, the hard work of negotiating a satisfactory departure from the EU, of which it has been a member for four decades, has begun. Talks are expected to last at least two years. In a closely-watched speech before the House of Lords last week, Queen Elizabeth II, attired in what many saw as a not-so-subtle EU flag-inspired gown and hat, said that her government’s priority “is to secure the best possible deal as the country leaves the European Union.”

That task, however, has recently been complicated by Prime Minister Theresa May’s humiliating loss of her government majority in the June 8 snap election. The disappointing outcome possibly signals waning public support for Brexit, which Brussels officials could very likely capitalize on and see as giving them increased leverage over making demands. A 100 billion pound exit fee, which has been hinted at, would be a decisive negotiation defeat.

What’s unclear at this point is what kind of Brexit the U.K. and the EU will pursue: a “hard” or “soft” exit. The former, favored by British nationalists, would strip the U.K. of all access to the single market and customs union. The country would effectively have full control of its borders and would also be required to assemble new trade deals from scratch.

A “soft” arrangement, on the other hand, would keep in place the country’s role in the European single market, meaning goods and services could still be traded tariff-free. As such, the U.K. would need to adhere to some basic rules involving the movement of goods, capital and people. Other European countries with similar arrangements include Iceland, Norway and Liechtenstein.

A piece in the Financial Times makes it clear that it’s this latter arrangement, the “soft” exit, that’s highly favored by British businesses of all sizes and from every sector. To be able to trade freely across borders without tariffs or other barriers, and to be able to hire skilled workers from the continent, would ensure that U.K. companies could remain competitive.

At this point, it’s really too early to tell which direction the two parties might take, but May’s crippling setback earlier this month will undoubtedly have a significant impact.

Below are five charts that illustrate where the U.K. has been in the 12 months following Brexit, both the good and bad—and where it could be headed next.

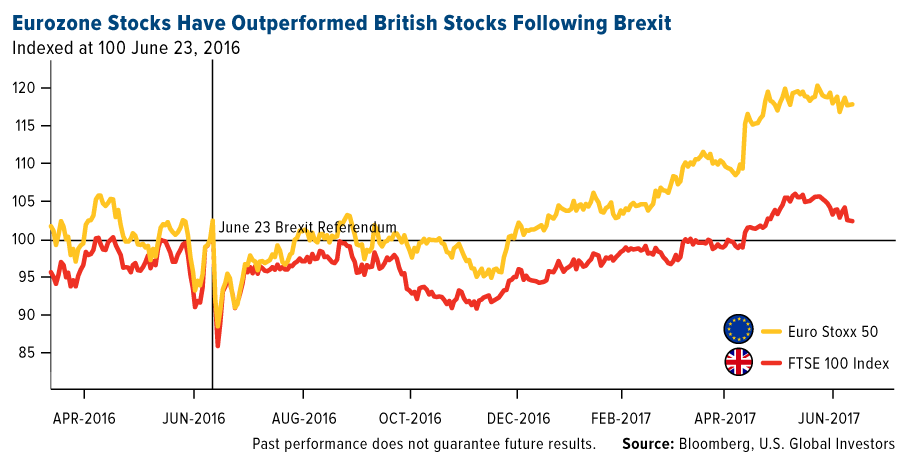

1. Stocks Head Higher

The benchmark British index, the FTSE 100 Index, has performed relatively well since last year’s referendum, despite skeptics’ pessimistic attitudes. Stocks have risen about 18 percent, even though they’ve trailed the Euro Stoxx 50, which has likely benefited from the euro’s rally since the start of the year.

Working in the FTSE 100’s favor is the weaker British pound, which has contracted 13.5 percent against the U.S. dollar as of today. A weaker national currency gives exporters a more competitive advantage and helps boost corporate earnings.

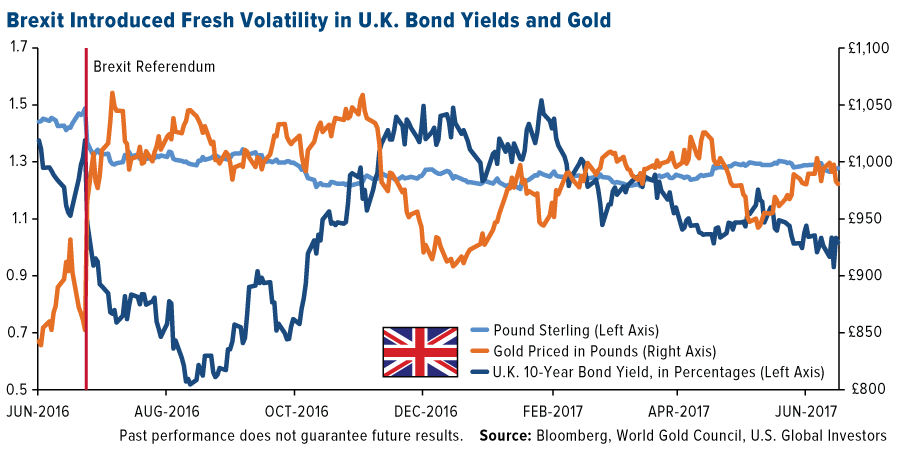

2. Gold Profits from Volatile Government Bonds

Also as a consequence of a weaker currency, gold priced in pounds is up close to 14 percent over the same period, from 861.2 pounds to 980.6 pounds. Supporting the yellow metal is low government bond yields, with nominal yields decaying to nearly 0.5 percent in August and September of last year.

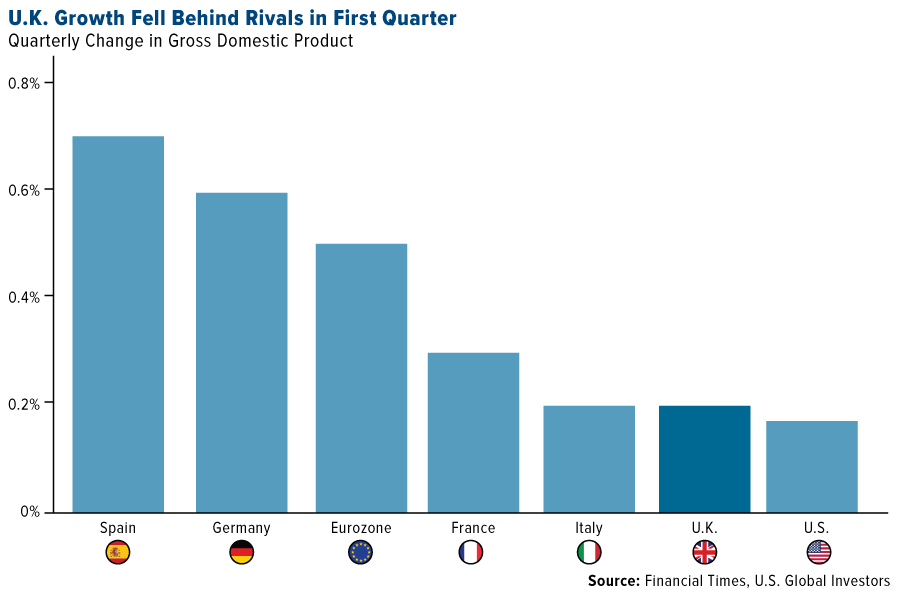

3. Economic Growth Stalls

GDP growth in the U.K. was worse than expected in the first quarter of 2017, gaining only 0.2 percent, its weakest showing in 12 months. The eurozone, by comparison, rose 0.5 percent in the March quarter.

CBI, the U.K.’s top business organization, recently announced expectations that the country’s economy will slow in the coming years. The group sees the U.K. growing at a weak 1.6 percent this year and 1.4 percent in 2018, with “domestic political turmoil” mostly to blame. Strength in manufacturing and exports could be tempered by higher-than-expected inflation and low wage growth.

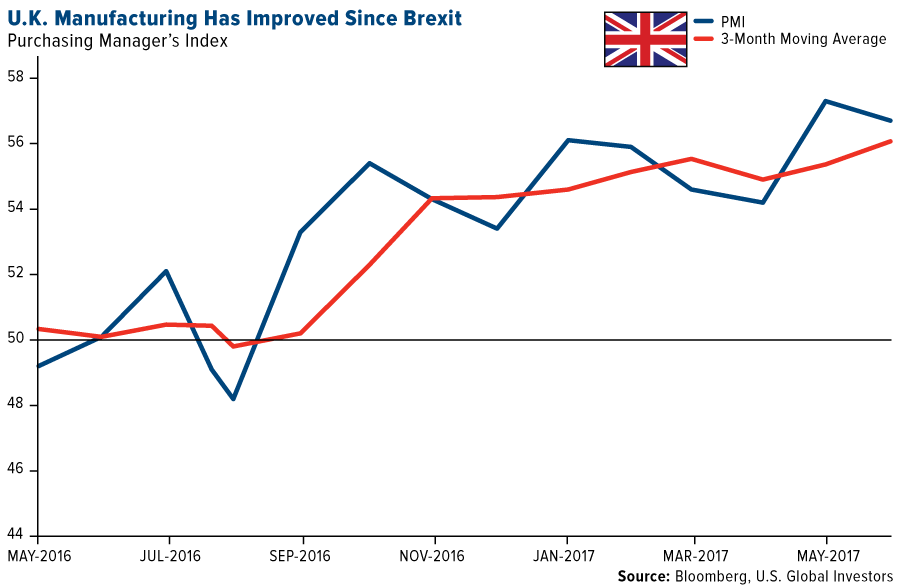

4. But Manufacturing Sees Further Growth

Many naysayers of the U.K. leaving the EU said demand for British-made goods would crumble, but the reverse has happened. The manufacturing sector remained strong and resilient in May, the most recent month of available data, with the PMI posting a 56.7. Output and new orders were strong, and job creation—its rate was positive for a straight 10 months—stood at a 35-month high, according to IHS Markit. What’s more, a survey of manufacturers found that 56 percent expected conditions to improve during the next 12 months.

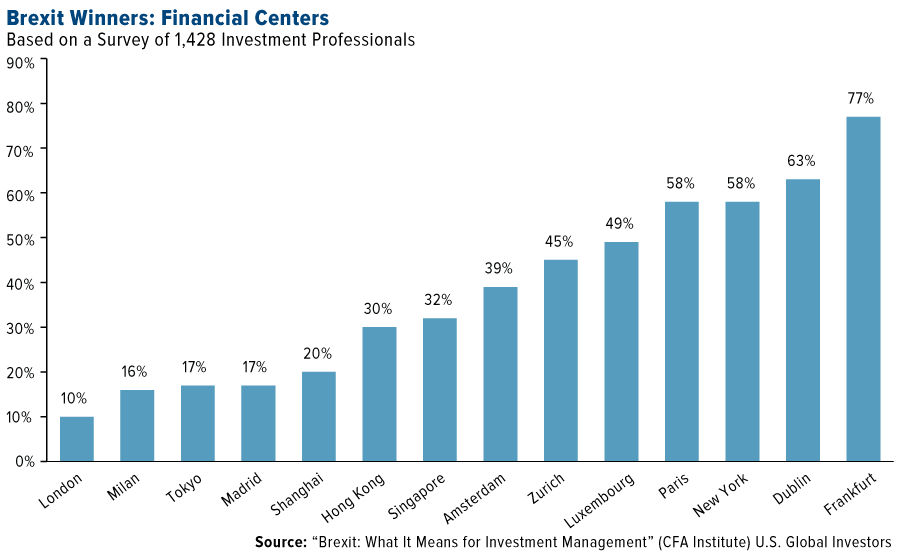

5. Financial Trouble Brewing?

Manufacturing might be looking good, but the financial sector is preparing for the worst. A survey conducted recently by the CFA Institute found that 70 percent of respondents said Brexit has deteriorated competitiveness of the market. Troublingly, 57 percent said they thought financial institutions based primarily in the U.K. would eventually reduce their presence in the U.K. because of added uncertainty. And when asked which world cities were poised to benefit from Brexit, participants placed London last at only 10 percent. Frankfurt, Dublin and New York topped the list of cities expected to benefit from financial professionals relocating from the U.K., should the country lose access to the single market.

A similar study conducted by financial consultancy firm Synechron found that, were the U.K. to leave the European single market, giant financial services firms with a presence in the U.K. could face some steep departures. JP Morgan Chase could lose up to 1,000 personnel; Morgan Stanley, 1,250; Bank of America, 1,386; Goldman Sachs, 1,603; and Citigroup, 2,000.

Again, we’re too early in the divorce process to make any firm predictions. We could be looking at two long years that hopefully aren’t as grueling and messy as some people fear.

For more award-winning market analysis, subscribe to my CEO blog Frank Talk!

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

The FTSE 100 Index is an index of the 100 companies listed on the London Stock Exchange with the highest market capitalization. The EURO STOXX 50 Index provides a Blue-chip representation of supersector leaders in the eurozone. The index covers 50 stocks from 12 eurozone countries: Austria, Belgium, Finland, France, Germany, Greece, Ireland, Italy, Luxembourg, the Netherlands, Portugal and Spain.

The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. None of the securities mentioned in the article were held by any accounts managed by U.S. Global Investors as of 3/31/2016.

Read more by Frank Holmes